Construction activity has declined for the third month running with still no sign of relief for the industry

The S&P March 2025 PMI’s headline figure reads 46.4, marginally up from February’s 44.6, but still below the 50.0 mark.

In spite of this slight recovery, the report still does not bode well for most sectors.

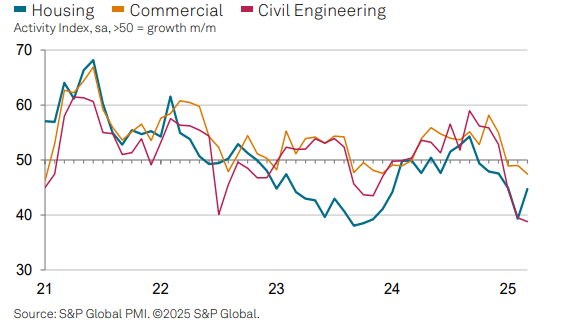

Civil engineering saw the largest fall in the S&P March 2025 PMIs

Civil Engineering saw an index figure of 38.8, marking its largest drop since October 2020, largely attributed to delays in new project decision-making and a weak pipeline of infrastructure work, with fewer projects to replace old ones in the works.

Both residential construction and commercial construction both remained within the negative area, at 44.7 and 47.4 respectively. Residential improved marginally over February’s number, but weak demand still dominated the responses to the index’s survey, while an easing of borrowing costs was a small positive for the sector. Commercial construction had a more modest decrease from the previous month, attributed by respondents to the pessimistic outlook of UK economic prospects and a rise in geopolitical uncertainty.

Construction order books have also been afflicted with a sluggish demand, with March following the trend of lower levels of new work throughout 2025, with companies noting a rise in competition and a fall in sales enquiries.

More pessimism comes from the lower rate of workloads, higher interest rates, and concerns with economic outlook, with events outside of the UK such as the Trump administration’s new global trade tariffs causing concern worldwide.

“A challenging month for UK construction”

Tim Moore, economics director at S&P Global Market Intelligence, said: “March data highlighted a challenging month for UK construction companies as sharply reduced order volumes continued to weigh on overall workloads.

“Civil engineering experienced the biggest setback as activity decreased to the greatest extent since October 2020. Survey respondents commented on subdued sales pipelines and a subsequent lack of infrastructure work to replace completed projects.

“Commercial work also saw a headwind from delayed decision-making on major projects, largely due to worries about the impact of rising global economic uncertainty. The downturn in residential construction activity nonetheless eased since February, providing a source of encouragement despite ongoing reports of sluggish demand conditions.

“Construction companies remained cautious about their year ahead growth prospects, as fewer sales conversions and a third successive monthly reduction in total new work hit confidence levels. Overall business optimism slipped to its lowest since October 2023.

“A lack of new projects, alongside pressure on margins from rising payroll costs, led to hiring freezes and the non-replacement of departing staff in March. The net result was the fastest pace of job shedding across the construction sector for nearly four-and-a-half years.”

The post S&P March 2025 PMI shows yet another contraction in activity appeared first on Planning, Building & Construction Today.