Re-flow explores what subcontractors need to prepare for as new standards come into effect on sustainability reporting

‘By strengthening data, governance, and risk processes now, even before the standard becomes mandatory, firms will be better positioned to meet the expectations of clients, investors, and communities’, wrote Louis Saunderson, sustainability analyst at Seddon in an article for New Civil Engineer.

His recommendations come alongside new updates on the UK Sustainability Reporting Standards (UK SRS S1 and S2).

These standards will be voluntary until 1 January 2027, and are set to shape the ‘procurement, financing, and planning decisions’ of major clients for the foreseeable future.

The rules tighten sustainability reporting for large clients and listed businesses that meet two of the following criteria:

- Turnover more than £54m

- Balance sheet over £27m

- More than 250 employees

This will inevitably impact contractors too. As compliance expectations rise, contractors will need to prove structured and reliable carbon data.

What’s the difference between SRS S1 and SRS S2 and how do they impact subcontractors?

The ‘UK Sustainability Reporting Standard S1: General Requirements for Disclosure of Sustainability related Financial Information’ (SRS S1) sets the general requirements for sustainability reporting.

- It covers all sustainability related risks and opportunities that could affect a company’s prospects.

- For subcontractors, this could include issues such as material sourcing risks, waste handling practices, biodiversity impacts on work sites, or workforce health and safety performance.

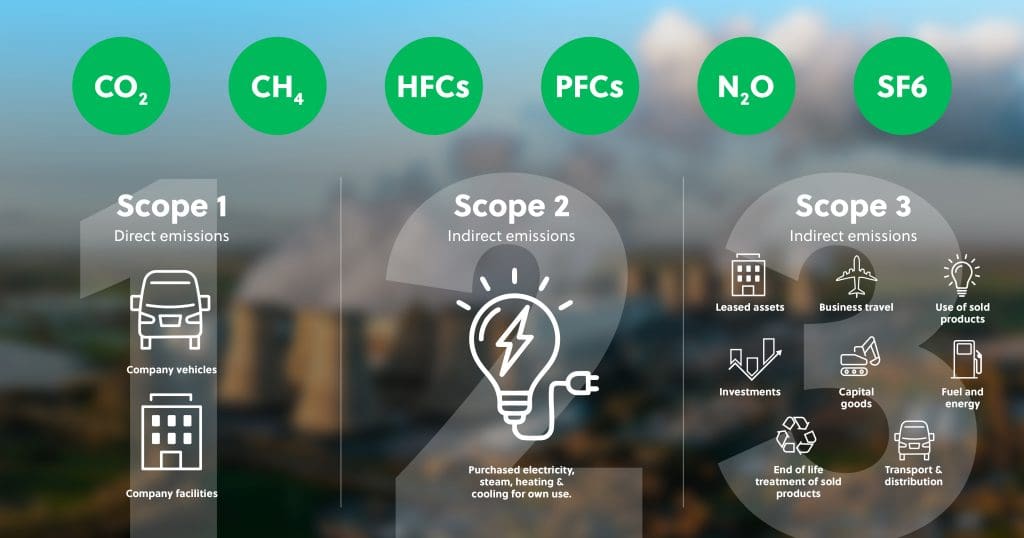

The ‘UK Sustainability Reporting Standard S2: Climate related Disclosures’ (SRS S2) focuses specifically on climate related disclosures. - It requires companies to report on climate risks, opportunities, and metrics, including Scope 1, 2 and (now on a ‘comply or explain’ basis) Scope 3 emissions.

- In practice, this means clients may ask subcontractors for data on fuel use from plant and vehicles, asphalt and concrete volumes, transport distances, or site energy consumption to support their climate reporting.

These increased disclosure measures will give ‘a clearer view of a company’s activities, risks and performance, enabling more informed dialogue and stronger accountability.’

A full list of impacted businesses can be found in a useful explainer on the TEAM (Energy Auditing Agency Ltd) website.

Latest updates

- While larger clients will be required to make climate related disclosures using the UK SRS S2 standard, Scope 3 emissions remain on a ‘comply or explain’ basis.

- Scope 3 relief reflects the difficulty companies still face in gathering reliable value chain data – but clients will expect clearer, more consistent information from their contractors.

- The same ‘comply or explain’ approach applies to wider sustainability topics under SRS S1, and much of the required data sits with subcontractors.

- Subcontractors can therefore expect a gradual increase in requests for structured information on carbon, environmental impacts, resource use, and site activity.

Ultimately, old reporting methods focused on proving compliance are giving way to new systems focused on providing better quality data. The aim is to harness insights capable of driving impactful strategy and innovation.

As for frameworks to help infrastructure teams understand how to generate better carbon data and deliver reductions – aligning with PAS 2080 is the obvious goal. And those who strengthen their evidence gathering now will be in a far better position to meet rising demands and stay competitive in future.

For a practical update on UK carbon initiatives, and for more insight into shifting data expectations across the sector, read the new Re-flow Infrastructure Carbon Report.

The post The shift to UK‑aligned sustainability reporting – what subcontractors need to prepare for appeared first on Planning, Building & Construction Today.