Amid persistent macroeconomic uncertainty and subdued client confidence, UK construction output recorded a fourth consecutive monthly decrease in April

However, the latest data from the S&P Global UK Construction PMI indicates early signs of stabilisation in activity, led by a relatively resilient residential sector.

A glimmer of stability in a contracting market

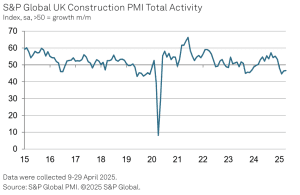

The headline PMI score edged up marginally to 46.6 in April, from 46.4 in March, marking the slowest rate of contraction in total activity since January. While the figure remains below the 50.0 threshold that separates growth from decline, the marginal rise is notable against a backdrop of declining commercial demand and curtailed civil engineering output.

“Output levels continued to slide in April, but the rate of decline eased to its slowest for three months,” said Tim Moore, economics director at S&P Global Market Intelligence.

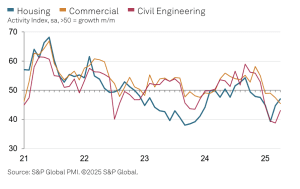

This stabilisation is rooted largely in residential building, where the PMI sub-index climbed to 47.1, the most robust reading so far in 2025. Although still signaling contraction, the residential sector outperformed both commercial construction (45.5) and civil engineering (43.1).

Commercial work falters as clients delay decisions

The commercial segment recorded its steepest drop since May 2020, reflective of widespread risk aversion and delays in client-side decision-making. Many survey respondents cited a “wait-and-see” attitude among stakeholders, particularly in light of mixed economic signals and uncertain policy pathways.

This hesitation has translated into real project delays, with new order volumes falling sharply, representing the second-fastest rate of decline since the pandemic-era lows of early 2020.

Procurement and employment trends: Reactive caution

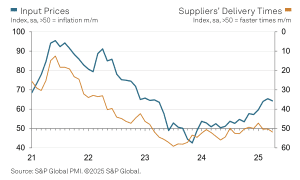

Procurement activity across the sector also declined sharply — the fastest drop in nearly five years — indicating supply chain recalibration in response to falling workloads. However, there was a silver lining: supplier delivery times continued to improve, reflecting less pressure on logistics and reduced material bottlenecks.

Employment numbers also shrank for the fourth straight month, though at a slower pace than March. The key drivers were voluntary departures not being replaced, and ongoing pay pressures that restrained hiring flexibility.

Cost pressures and price volatility remain in focus

Despite weaker demand, cost inflation remains elevated, particularly for concrete products, insulation, and timber. The report flagged widespread attempts by suppliers to pass on rising payroll costs, even as firms report easing fuel prices and logistical improvements.

Input price inflation moderated only slightly from March’s 26-month peak, underscoring that structural inflation in the materials market remains a strategic challenge for contractors and developers.

Cautious optimism on the horizon

Encouragingly, the forward-looking indicators signal a moderate uplift in sentiment. 41% of firms now anticipate higher output over the next 12 months, compared to 18% expecting a decline. The improvement in business optimism is the strongest since December 2024, with many firms expressing confidence in a recovery in residential workloads.

This bifurcated outlook — confidence in housing contrasted with commercial hesitation — will likely guide resource allocation and investment strategies in the coming quarters.

Strategic takeaways for senior construction leaders

| Key Indicator | Value (April 2025) | Trend |

|---|---|---|

| Total Activity Index (PMI) | 46.6 | Slowest contraction in 3 months |

| Residential Activity | 47.1 | Most resilient segment |

| Commercial Activity | 45.5 | Sharpest drop since May 2020 |

| Civil Engineering | 43.1 | Continues to weaken |

| Purchasing Activity | ▼ | Steepest fall in 5 years |

| Input Cost Inflation | ▲ | Near record levels |

| Business Confidence (12 months) | ↑ | Highest since Dec 2024 |

Industry reactions

Lauren Pamma, head of energy & infrastructure at Aldermore Bank, comments on the S&P Global UK Construction PMI data:

“It’s another month of output decline, and while most categories of construction work saw weaker activity performances, the rate of decline eased to its slowest for three months. Businesses are feeling the burden of April’s rises in National Insurance Contributions and the National Minimum Wage, which has meant rising payroll costs. Stagnant demand, rising interest rates and delayed decision making on new projects seem to be continuing to take its toll as well.

“We’re beginning to see the fallout from the ongoing cross-border tariff war which will no doubt disrupt supply chains and impact prices further moving forwards. The outlook still remains unclear, and with developments emerging every day, SMEs will be monitoring the geopolitical landscape closely to see how the construction sector will be impacted.”

Gareth Belsham, director of Bloom Building Consultancy, commented:

“This is a reset rather than a recovery. After much of the construction industry endured a miserable start to the year, April’s slightly improved data represents fragile progress. Yet for all the sighs of relief, we’re not even in ‘leveling off’ territory yet. Output is still falling in residential, commercial and infrastructure construction.

“But the rate of decline has eased considerably in housebuilding, with many residential developers anticipating an uptick in buyer demand later this year as falling interest rates make mortgages more affordable. Yet things are far less benign on the commercial property side, with the pace of decline here back up to levels last seen during the depths of the first Covid lockdown.

“New orders are becoming increasingly scarce as economic uncertainty leads many commercial developers to hover at the ‘go / no go’ threshold. As long as business sentiment remains this weak, there’s a risk that the number of paused projects will increase.

“Yet for all that, a majority of contractors are upbeat about the future, with 41% predicting that business will improve over the next 12 months – the highest level of industry optimism seen so far this year.

“That optimism is strongest amongst housebuilders, who are hoping that a combination of lower interest rates – which make it cheaper for developers to buy land and fund projects – and the Government’s long awaited easing of planning rules, could unleash a surge in residential schemes.

“Overall the glass is half full, but only just.”

Final word: A sector in tactical pause

The April 2025 PMI report paints a picture of a construction industry that is neither rebounding nor in freefall — but in tactical pause. Senior decision-makers would be wise to interpret the current contraction as cyclical and project-specific, not indicative of a structural industry retreat.

As the residential sector shows early signs of recovery and procurement/supply lines improve, the focus now shifts to commercial sector recalibration and the management of inflationary risk in input costs.

The post UK Construction PMI April 2025: Resilience in residential despite continued output decline appeared first on Planning, Building & Construction Today.